The Data Suggests a Very Different Story

For years, a dominant narrative has shaped Australia’s housing debate:

“Investors are buying up all the properties and pushing out first home buyers.”

It’s a simple explanation — and simple explanations spread easily — but when we examine long‑term data from South Australia and New South Wales, a very different picture emerges. The evidence suggests that the housing crisis may be driven less by investor activity and far more by a 30‑year decline in public housing stock across multiple states (AIHW 2023).

The graphs below, drawn from reconstructed AIHW public housing data and state bond lodgement rent trends, illustrate this structural shift clearly.

South Australia: A 30‑Year Divergence Between Public Housing and Private Rents

The South Australian graph shows two unmistakable trends:

- Public housing stock has fallen from around 60,000 dwellings in 1995 to roughly 34,000 in 2025 (AIHW 2023).

- Median private rent has risen from around $145/week to more than $450/week over the same period (CBS SA 2024).

These lines move in opposite directions — one declining steadily, the other rising sharply.

This pattern aligns with broader national findings that public housing as a share of total dwellings has halved since the mid‑1990s (MFAA 2024; RBA 2024). As governments reduce their direct role in providing housing, demand shifts into the private rental market, increasing competition for a limited pool of dwellings.

This is a structural supply issue, not a behavioural one.

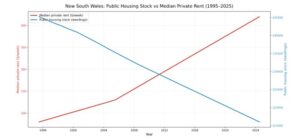

New South Wales: The Same Pattern at a Larger Scale

New South Wales shows the same long‑term divergence:

- Public housing stock has declined from around 145,000 dwellings in 1995 to approximately 115,000 in 2025 (AIHW 2023).

- Median private rent has increased from roughly $180/week to more than $425/week (NSW Fair Trading 2024).

Again, the relationship is clear:

as public housing availability falls, private rents rise.

If investors were the primary cause of the crisis, we would expect to see:

- a sharp increase in investor share of housing

- a reduction in rental supply

- rent increases independent of public housing trends

But the data does not support this. Investor lending has fluctuated but remained broadly stable as a share of total lending over the past two decades (RBA 2024). Meanwhile, the number of rental properties has grown, not shrunk (ABS 2024).

The only major category of housing that has consistently declined is public housing.

Why the “Blame the Investor” Narrative Falls Short

This is not to say investors have no influence on the market — they do. But the idea that they are the primary cause of the housing crisis is not supported by long‑term evidence.

- Investor activity has not increased in a way that explains 30 years of rent growth

Investor lending cycles up and down, but the long‑term trend is relatively stable (RBA 2024).

- Investor purchases typically add to rental supply

When an investor buys a property, it becomes a rental.

When a government sells or demolishes a public housing dwelling, it is often removed from the rental pool entirely (AIHW 2023).

- Public housing stock has been shrinking for decades

This is the most consistent trend across states.

The decline is not marginal — it is structural and long‑term.

- More households are being pushed into the private rental market

When public housing is unavailable, low‑income households must compete in the private market, increasing demand and driving up rents (CoreLogic 2024).

The graphs make this dynamic visible.

A More Accurate Explanation: Structural Divestment, Not Investor Behaviour

The combined evidence from SA and NSW suggests:

- Public housing stock has declined significantly over 30 years.

- Private rents have risen sharply over the same period.

- These trends move in opposite directions — consistently and predictably.

This does not mean investors have no impact.

But it does mean the dominant narrative — that investors are the primary cause of the crisis — is incomplete.

A more accurate explanation is this:

Australia’s housing crisis is strongly linked to a long‑term divestment from public housing, which has shifted demand into the private rental market and placed upward pressure on rents.

This is a structural issue, not an individual one.

Where This Leaves the Policy Conversation

If Australia wants to meaningfully address housing affordability, the data suggests that focusing solely on investor behaviour will not solve the underlying problem.

Rebuilding or stabilising public housing stock — or at least halting its decline — would likely have a more significant impact on rental affordability than any investor‑targeted policy alone.

The graphs from SA and NSW make this clear:

when public housing declines, private rents rise.

It’s time the national conversation reflected that reality.